In short ⚡

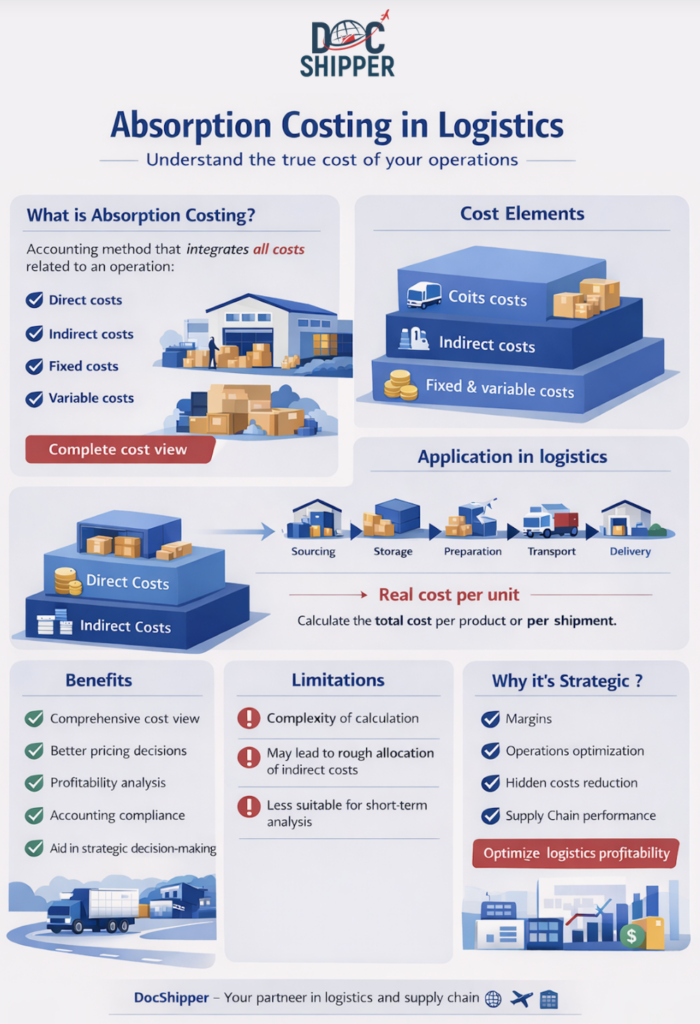

Absorption costing is an accounting method that assigns all manufacturing costs—both variable and fixed—to individual product units. This comprehensive approach includes direct materials, direct labor, variable overhead, and fixed overhead in the cost of goods sold, ensuring full cost recovery in product pricing and inventory valuation.

Introduction

Many businesses struggle with accurate product costing, leading to pricing errors and inventory misstatements. Understanding absorption costing is essential for international trade operations where precise cost allocation impacts customs valuations, transfer pricing, and profitability analysis.

In global logistics and manufacturing, absorption costing provides the foundation for compliant financial reporting under GAAP and IFRS standards. This method ensures that every product unit reflects its true production burden, critical for import/export documentation and tax compliance.

- Comprehensive cost allocation: Captures all manufacturing expenses in product costs

- Regulatory compliance: Required for external financial reporting in most jurisdictions

- Inventory valuation: Reflects full production costs in balance sheet assets

- Pricing foundation: Ensures all costs are recovered through sales prices

- Profitability analysis: Provides accurate gross margin calculations per product line

In-Depth Analysis & Expert Insights

Absorption costing operates on the principle that fixed manufacturing overhead represents a necessary cost of production that should be distributed across all units manufactured. Unlike variable costing, which treats fixed overhead as a period expense, absorption costing capitalizes these costs into inventory until products are sold.

The calculation involves determining a predetermined overhead rate by dividing estimated annual fixed overhead by expected production volume. This rate is then applied to actual production units. For instance, if annual fixed overhead totals $500,000 and expected production is 100,000 units, the overhead rate becomes $5 per unit.

Under Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), absorption costing is mandatory for external reporting. The Financial Accounting Standards Board requires this method to match production costs with revenues in the period products are sold, adhering to the matching principle.

The method creates a direct link between production volume and profitability. Higher production volumes spread fixed costs across more units, reducing per-unit costs and increasing reported profits when inventory levels rise. This relationship has significant implications for management decisions and performance evaluation.

At DocShipper, we assist clients in accurately calculating absorption costs for customs declarations and transfer pricing documentation, ensuring compliance with international trade regulations while optimizing duty assessments.

The distinction between product costs and period costs is fundamental. Product costs (direct materials, direct labor, variable overhead, fixed overhead) are inventoriable and flow through cost of goods sold when products sell. Period costs (selling, administrative expenses) are expensed immediately, never becoming part of inventory valuation.

Practical Examples & Cost Data

Consider a manufacturing scenario where a company produces electronic components for international distribution. The following cost structure illustrates absorption costing application:

| Cost Component | Per Unit | Annual Total (50,000 units) |

|---|---|---|

| Direct Materials | $15.00 | $750,000 |

| Direct Labor | $8.00 | $400,000 |

| Variable Manufacturing Overhead | $4.00 | $200,000 |

| Fixed Manufacturing Overhead | $6.00 | $300,000 |

| Total Absorption Cost | $33.00 | $1,650,000 |

In this example, each unit carries $33.00 in total manufacturing cost under absorption costing. If the company sells 40,000 units at $50 each, the gross profit calculation becomes:

- Sales Revenue: 40,000 units × $50 = $2,000,000

- Cost of Goods Sold: 40,000 units × $33 = $1,320,000

- Gross Profit: $2,000,000 – $1,320,000 = $680,000

- Ending Inventory: 10,000 units × $33 = $330,000 (capitalized on balance sheet)

- Fixed Overhead in Inventory: 10,000 units × $6 = $60,000 (deferred expense)

The critical insight: $60,000 of fixed overhead remains in inventory rather than being expensed immediately. This deferred recognition increases reported net income compared to variable costing, where all fixed overhead would be expensed in the current period regardless of sales volume.

For international shipments, absorption costing affects customs valuation declarations. When DocShipper prepares import documentation, we ensure that the declared value reflects the full absorption cost, including allocated fixed overhead, to comply with WTO valuation agreements and avoid undervaluation penalties.

A comparative scenario demonstrates the impact of production volume changes. If production increases to 60,000 units while fixed overhead remains $300,000:

- New fixed overhead rate: $300,000 ÷ 60,000 = $5.00 per unit

- New total absorption cost: $15 + $8 + $4 + $5 = $32.00 per unit

- Cost reduction: $1.00 per unit due to overhead absorption efficiency

DocShipper Platform

Cut logistics costs. Not corners.

See exactly where your logistics costs are bleeding — and how to fix it. Book your expert demo.

Conclusion

Absorption costing remains the cornerstone of manufacturing cost accounting, ensuring comprehensive expense allocation and regulatory compliance. Mastering this method enables accurate pricing, inventory management, and financial reporting across international operations.

Need expert guidance on cost allocation for your import/export operations? Contact DocShipper for specialized support in logistics cost management and customs compliance.

📚 Quiz

Test Your Knowledge: Absorption Costing

Q1 — Which of the following best defines absorption costing?

Q2 — Under absorption costing, what happens to fixed manufacturing overhead allocated to unsold units at the end of a period?

Q3 — A manufacturer has $300,000 in fixed overhead and produces 60,000 units. Using absorption costing, what is the fixed overhead cost per unit, and what happens to that rate if production rises to 75,000 units (fixed overhead unchanged)?

🎯 Your Result

📞 Free Quote in 24hFAQ | Absorption Costing: Definition, Calculation & Practical Examples

Absorption costing includes fixed manufacturing overhead in product costs, while variable costing treats fixed overhead as a period expense. This creates different inventory valuations and profit figures when production and sales volumes differ.

GAAP and IFRS mandate absorption costing because it matches all production costs with revenues in the period products are sold, adhering to the matching principle and providing a complete picture of manufacturing expenses.

Inventory values are higher under absorption costing because they include allocated fixed overhead. This capitalized overhead becomes an expense only when products sell, deferring expense recognition compared to variable costing.

Yes, managers can increase reported profits by overproducing inventory, spreading fixed costs across more units and deferring expense recognition. This practice, called "inventory buildup," inflates short-term profits without increasing actual sales.

The formula includes direct materials, direct labor, variable manufacturing overhead, and fixed manufacturing overhead. Non-manufacturing costs like selling and administrative expenses are excluded from product costs.

Divide estimated annual fixed manufacturing overhead by expected production volume. For example, $600,000 fixed overhead ÷ 120,000 expected units = $5.00 fixed overhead per unit.

Fixed overhead allocated to unsold units remains capitalized in ending inventory on the balance sheet. This deferred expense recognition increases net income compared to expensing all fixed overhead immediately.

Customs valuations must reflect the full absorption cost of imported goods, including allocated fixed overhead. Undervaluing shipments by excluding these costs can result in penalties and duty adjustments.

Absorption costing primarily applies to manufacturing operations with inventoriable products. Service businesses typically use different costing methods since services cannot be inventoried and costs are generally period expenses.

Absorption costing can obscure the relationship between costs, volume, and profit because fixed costs per unit change with production levels. This makes break-even analysis and short-term decision-making more complex.

Companies typically recalculate overhead rates annually based on budgeted costs and expected production. However, significant changes in production capacity, cost structure, or operations may warrant mid-year adjustments.

Yes, activity-based costing (ABC) can refine absorption costing by allocating overhead based on cost drivers rather than simple volume measures. This hybrid approach provides more accurate product costs while maintaining full absorption principles.

Need Help with

Logistics or Sourcing ?

First, we secure the right products from the right suppliers at the right price by managing the sourcing process from start to finish. Then, we simplify your shipping experience - from pickup to final delivery - ensuring any product, anywhere, is delivered at highly competitive prices.

Fill the Form

Prefer email? Send us your inquiry, and we’ll get back to you as soon as possible.

Contact us

{kind=link}