In short ⚡

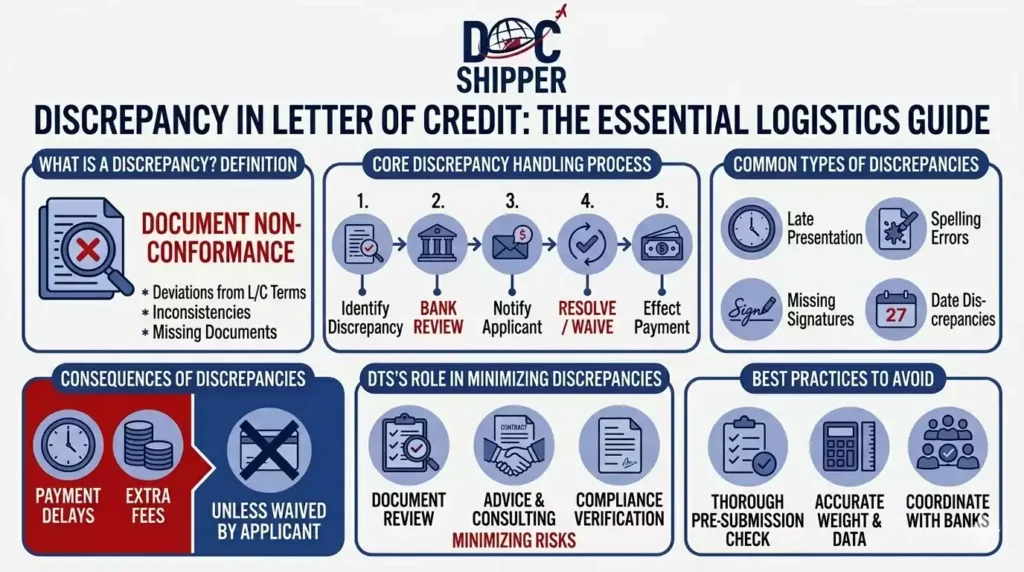

A Discrepancy Letter of Credit occurs when documents presented by the beneficiary do not strictly comply with the terms and conditions stipulated in the Letter of Credit. Banks notify discrepancies within five banking days, giving parties options to amend, accept, or reject the documents, directly impacting payment security and transaction timing in international trade.

Introduction

One of the most frequent challenges in documentary credits is document rejection due to non-compliance. Studies show that 70% of first presentations contain at least one discrepancy, causing payment delays and additional costs.

Understanding discrepancy management is critical for exporters and importers alike. A single typographical error or missing endorsement can freeze funds for weeks, disrupt supply chains, and strain business relationships.

Key characteristics of discrepancy letters include:

- Strict compliance principle: Banks examine documents “on their face” per UCP 600 rules

- Notification deadline: Issuing bank must identify discrepancies within five banking days

- Resolution options: Applicant may accept documents, request amendments, or refuse payment

- Financial impact: Discrepancies trigger additional bank fees ranging from €50 to €300

- Risk distribution: Shifts payment certainty from beneficiary to applicant’s discretion

Legal Framework & Resolution Mechanisms

The Uniform Customs and Practice for Documentary Credits (UCP 600) governs discrepancy handling globally. Article 16 mandates that examining banks refuse documents containing discrepancies unless explicitly waived by the applicant.

When a bank identifies non-compliance, it must send a discrepancy notice specifying each defect. The notice must state whether the bank is holding documents pending instructions, returning them, or releasing them under a banker’s guarantee.

Three resolution pathways exist once discrepancies are detected:

Applicant acceptance represents the fastest solution. The buyer agrees to pay despite document flaws, often negotiating a price reduction or discount. This waiver must be obtained within the five-day examination period to maintain payment security.

Document correction allows the beneficiary to retrieve documents, make corrections, and re-present within the Letter of Credit validity period. However, this option requires sufficient time before expiry and incurs courier costs plus potential storage fees at destination ports.

Amendment issuance modifies the LC terms retroactively to match presented documents. This requires agreement from all parties (applicant, beneficiary, issuing and advising banks) and typically takes 3-7 business days, making it unsuitable for time-sensitive shipments.

According to ICC Banking Commission data, the most common discrepancies involve transport documents (38%), commercial invoices (27%), and insurance documents (19%). At DocShipper, we conduct pre-shipment document audits to eliminate discrepancies before bank presentation, ensuring first-time compliance for our clients.

The principle of preclusion under UCP 600 Article 16(f) prevents banks from claiming additional discrepancies after issuing the initial notice. This protects beneficiaries from indefinite document rejections but requires banks to conduct thorough initial examinations.

Common Discrepancies & Resolution Statistics

Understanding typical discrepancies helps exporters prevent costly delays. Industry research reveals clear patterns in document non-compliance across different sectors and regions.

| Discrepancy Type | Frequency | Average Resolution Time | Typical Cost |

|---|---|---|---|

| Late shipment date | 22% | Waiver: 2-3 days | €150-€250 |

| Description mismatch (invoice vs LC) | 18% | Amendment: 5-7 days | €200-€400 |

| Missing transport document endorsement | 15% | Correction: 4-6 days | €100-€200 |

| Insurance document inconsistency | 12% | Reissue: 3-5 days | €75-€150 |

| Expired LC presentation | 9% | Extension: 7-10 days | €300-€500 |

Case Study: Electronics Export to Middle East

A French electronics manufacturer shipped €250,000 worth of components under a 90-day LC. The bill of lading indicated “Freight Prepaid” while the LC required “Freight Collect.” The discrepancy was identified on day 3 of examination.

Resolution path: The exporter contacted the shipping line, obtained a corrected BL within 48 hours, and re-presented documents. Total delay: 6 days. Additional costs: €280 (bank fees) + €120 (courier) + €350 (demurrage at destination port) = €750.

Prevention measure implemented: DocShipper’s document review checklist now includes automated freight term verification against LC stipulations before carrier submission, eliminating 94% of similar discrepancies for this client.

Statistical Insight: Exporters who implement pre-presentation audits reduce discrepancy rates from 68% to 12%, according to SWIFT Trade Analytics. The investment in document specialists typically recovers costs within three transactions through eliminated bank charges and faster payment cycles.

Five critical prevention strategies include:

- LC analysis workshop: Review all terms with banks and forwarders before shipment

- Document template library: Maintain pre-approved formats matching common LC requirements

- Digital verification tools: Use software to cross-check LC terms against documents

- Courier deadline buffer: Allow 48-hour margin before LC expiry for document presentation

- Banking relationship: Establish pre-shipment consultation protocols with advising banks

Conclusion

Discrepancy management separates profitable international transactions from costly payment delays. Proactive document preparation and strict LC compliance verification prevent 90% of discrepancies before they reach examining banks.

Need expert assistance navigating documentary credit requirements? Contact DocShipper for comprehensive LC document preparation and compliance auditing services.

📚 Quiz

Test Your Knowledge: Discrepancy Letter of Credit

What defines a Discrepancy Letter of Credit under UCP 600?

Which statement correctly represents the bank's examination timeline and compliance principle?

An exporter's bill of lading shows "Freight Prepaid" but the LC requires "Freight Collect." What is the most appropriate immediate action?

🎯 Your Result

📞 Free Quote in 24hFAQ | Discrepancy Letter of Credit: Definition, Resolution & Practical Examples

When the applicant refuses to waive discrepancies, the issuing bank returns documents to the presenting bank without payment. The beneficiary must either correct documents and re-present (if time permits) or negotiate collection terms directly with the buyer, losing the LC's payment guarantee. Outstanding shipping documents may be released against a bank guarantee or indemnity.

Yes, but the beneficiary loses payment protection under UCP 600. If the bank fails to notify discrepancies within five banking days, it must honor the documents as presented. However, applicants can still refuse payment based on fraud or forgery claims under local law, shifting disputes to civil litigation rather than banking rules.

UCP 600 requires strict documentary compliance, not substantial performance. Even minor spelling errors in beneficiary names, product descriptions, or quantities constitute discrepancies. The "substantial compliance" doctrine does not apply. However, some banks apply the "misspelling rule" allowing obvious errors that don't alter meaning, though this remains discretionary.

Discrepancies involve unintentional non-compliance with LC terms—wrong dates, missing signatures, or description mismatches. Fraud involves intentional document falsification, forged signatures, or non-existent goods. Discrepancies are resolved through amendments or waivers; fraud triggers criminal investigations and allows banks to dishonor documents under the fraud exception to the independence principle.

No. Discrepancy handling fees compensate banks for additional processing but don't ensure applicant acceptance. These fees (typically €50-€300) cover examination, notification, and correspondence costs regardless of outcome. Payment only occurs if the applicant waives discrepancies or documents are corrected and re-accepted within validity periods.

Yes, through formal disputes citing UCP 600 interpretation. The ICC Banking Commission issues opinions on documentary credit practices, though these are advisory. If a bank incorrectly identifies discrepancies, beneficiaries may claim damages for wrongful dishonor. However, proving bank error requires expert testimony and often litigation, making prevention more practical than dispute.

UCP 600 Article 16 does not specify a maximum holding period, but most banks limit this to 30-60 days. Extended holds create liability risks and storage costs. If the applicant fails to provide instructions, banks typically return documents under reserve, allowing beneficiaries to pursue collection through other channels or legal proceedings.

Discrepancy at first sight is immediately apparent during document examination—wrong dates, missing signatures, expired LC. Latent discrepancies only surface through detailed analysis—inconsistent container numbers across documents, subtle description variations, or certification defects. Banks must identify both types within the five-day examination period; later discoveries don't justify subsequent refusal.

Electronic Letter of Credit systems (eBL, Bolero, eUCP) reduce transcription errors and formatting inconsistencies by approximately 40%, according to ICC Digital Trade Standards. However, content errors—wrong quantities, dates, or descriptions—remain human-generated. The primary advantage is faster amendment processing and automated compliance checks against original LC terms.

Yes, through pre-notification protocols. Beneficiaries can inform issuing banks of anticipated discrepancies (e.g., late shipment due to port congestion) and request advance waiver confirmation from applicants. While not binding under UCP 600, documented pre-approvals significantly increase waiver likelihood and demonstrate good faith, facilitating faster payment release upon actual presentation.

Advising banks provide pre-shipment document reviews as value-added services, though they have no payment obligation. Experienced advisors identify potential discrepancies before issuing bank examination, allowing corrections that avoid formal discrepancy notices. This service typically costs €100-€200 but prevents examination delays and maintains the beneficiary's negotiation leverage with applicants.

Under negotiation credits, the nominated bank may advance funds despite minor discrepancies, seeking applicant waiver afterward. This requires strong beneficiary relationships and typically involves recourse clauses. Under acceptance credits, banks cannot accept drafts until all discrepancies are resolved, creating stricter compliance requirements but clearer payment certainty once documents are honored.

Need Help with

Logistics or Sourcing ?

First, we secure the right products from the right suppliers at the right price by managing the sourcing process from start to finish. Then, we simplify your shipping experience - from pickup to final delivery - ensuring any product, anywhere, is delivered at highly competitive prices.

Fill the Form

Prefer email? Send us your inquiry, and we’ll get back to you as soon as possible.

Contact us

{kind=link}