In short ⚡

The barter system is a method of exchange where goods or services are directly traded without using money as an intermediary. In international trade, it enables businesses to conduct transactions through countertrade agreements, particularly valuable when currency shortages, capital controls, or trade restrictions limit traditional payment methods.

Introduction

Many companies face payment challenges when expanding into emerging markets with unstable currencies or strict foreign exchange controls. The barter system offers a strategic alternative to conventional monetary transactions.

In global logistics and international trade, barter remains relevant for specific scenarios. Companies use it to preserve cash flow, enter restricted markets, or liquidate excess inventory.

- Direct exchange: No currency intermediary required

- Countertrade mechanism: Bilateral agreements between trading partners

- Valuation complexity: Requires precise goods/services assessment

- Documentation requirements: Contracts must specify exchange ratios and delivery terms

- Tax implications: Transactions subject to fair market value reporting

Understanding barter mechanics is essential for freight forwarders and importers navigating non-traditional payment structures. At DocShipper, we regularly assist clients in structuring compliant countertrade operations that meet customs and regulatory requirements.

Mechanisms & Trade Expertise

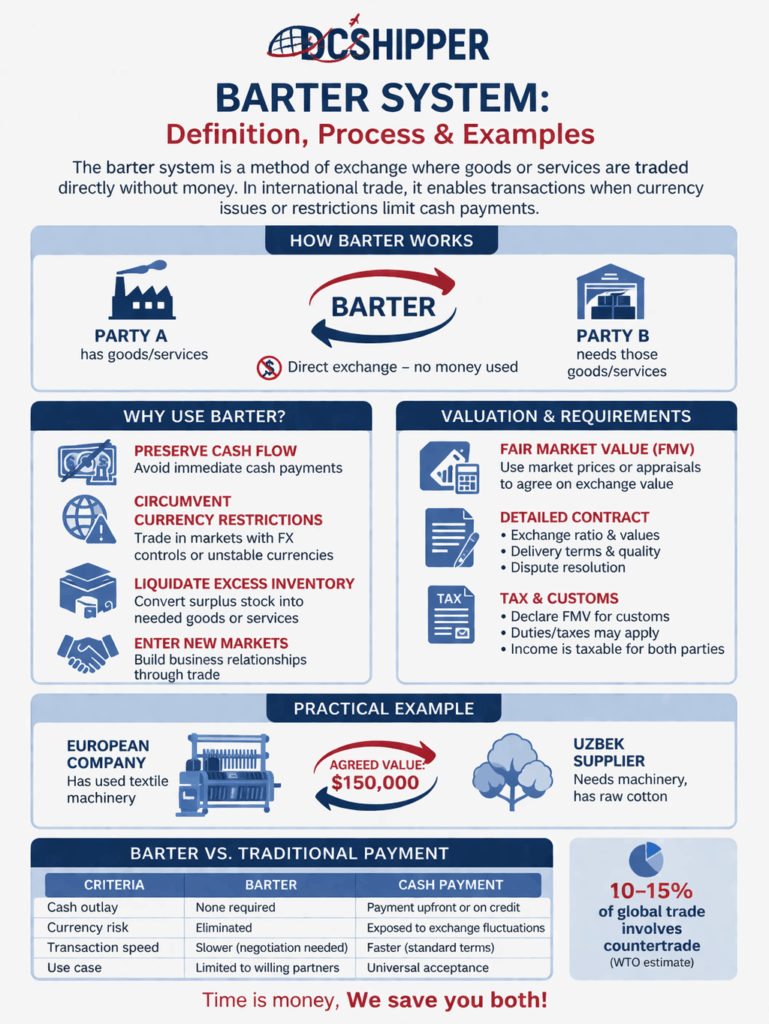

The barter system operates through direct negotiation between parties who agree on the relative value of exchanged goods. Unlike monetary transactions, both parties must identify mutual needs before executing the trade.

Valuation methodology represents the primary technical challenge. Companies typically use fair market value (FMV) as the baseline, referencing comparable sales data or professional appraisals. The exchange ratio must reflect current market conditions to satisfy customs authorities.

From a legal perspective, countertrade contracts require specific clauses addressing delivery schedules, quality standards, and dispute resolution. The International Chamber of Commerce provides arbitration frameworks commonly used in cross-border barter agreements.

Customs classification follows standard procedures despite the absence of monetary payment. Importers must declare the transaction value based on FMV, and duties/taxes apply as they would for purchased goods. Documentation must include detailed invoices showing the agreed valuation.

Tax reporting obligations vary by jurisdiction but generally require both parties to recognize income equal to the FMV of goods received. The IRS and equivalent authorities treat barter as taxable transactions, making accurate record-keeping critical.

At DocShipper, we verify all valuation documentation during the customs clearance process to prevent delays. Our compliance team ensures barter transactions meet both origin and destination country requirements, particularly for controlled commodities.

Concrete Examples & Trade Data

Real-world barter applications demonstrate the system’s utility in specific trade scenarios. Understanding these cases helps businesses identify opportunities for non-monetary exchanges.

Comparative Analysis: Barter vs. Traditional Payment

| Criteria | Barter System | Monetary Payment |

|---|---|---|

| Cash Flow Impact | No immediate cash outlay required | Requires available capital or credit |

| Transaction Speed | Slower (negotiation + valuation) | Faster (standardized pricing) |

| Currency Risk | Eliminated | Subject to exchange rate fluctuations |

| Documentation Complexity | High (detailed valuation needed) | Standard (invoice + payment proof) |

| Market Applicability | Limited to willing counterparties | Universal acceptance |

Use Case: Manufacturing Equipment Exchange

Scenario: A European textile manufacturer needs raw cotton worth $150,000 but faces currency restrictions when trading with an Uzbek supplier.

Solution: The parties negotiate a barter agreement where the European company provides used textile machinery valued at $150,000 in exchange for 75 tons of cotton.

Valuation Process:

- Machinery appraised by certified evaluator: $148,000–$152,000 range

- Cotton priced at $2,000/ton (current market rate): $150,000 total

- Exchange ratio agreed: 1:1 based on FMV

- Both parties declare $150,000 transaction value to customs

- Import duties calculated on declared value per HS code classification

Outcome: The European company preserves $150,000 in cash while obtaining necessary raw materials. The Uzbek supplier acquires production equipment without foreign currency expenditure.

According to World Trade Organization data, countertrade arrangements (including barter) account for approximately 10-15% of global trade volume, with higher concentrations in Central Asia, Africa, and Latin America where currency volatility remains significant.

Conclusion

The barter system provides a viable alternative for international trade when monetary transactions face obstacles. Proper valuation and documentation ensure regulatory compliance while preserving commercial flexibility.

Need assistance structuring a countertrade operation? Contact DocShipper for expert guidance on barter logistics and customs compliance.

📚 Quiz

Test Your Knowledge: Barter System

Q1 — What is the defining characteristic of the barter system in international trade?

Q2 — A common misconception about barter transactions is that they are tax-free. What is the correct interpretation?

Q3 — A European manufacturer wants to acquire raw cotton from an Uzbek supplier but faces strict currency controls. Which approach correctly applies the barter system?

🎯 Your Result

📞 Free Quote in 24hFAQ | Barter System: Definition, Calculation & Concrete Examples

Yes, barter is legal worldwide when properly documented. Transactions must comply with customs regulations, tax reporting requirements, and trade sanctions. Both parties must declare fair market value for duty assessment purposes.

Customs apply duties based on the fair market value of imported goods, regardless of payment method. Importers must provide valuation documentation supporting the declared transaction value, typically through independent appraisals or comparable sales data.

Essential documents include a countertrade agreement specifying exchange terms, valuation reports establishing fair market value, commercial invoices showing transaction details, and standard shipping documents (bill of lading, packing list, certificates of origin).

No. Tax authorities treat barter as taxable transactions. Both parties must report income equal to the fair market value of goods/services received. Attempting to undervalue exchanges constitutes tax evasion and carries severe penalties.

Agriculture, commodities trading, manufacturing equipment, media advertising, and technology sectors frequently employ barter. Industries with high inventory carrying costs or those operating in currency-restricted markets find barter particularly advantageous.

Barter preserves working capital by eliminating immediate cash outlays. However, it requires careful inventory management since exchanged goods must be usable or resalable. Companies should assess liquidity impact before committing to large barter agreements.

Primary risks include valuation disputes, quality discrepancies, delivery delays, and difficulty liquidating received goods. Comprehensive contracts with arbitration clauses and third-party inspections mitigate these concerns. Currency risk is eliminated but replaced by commodity price volatility.

The physical logistics remain identical to paid shipments. However, forwarders must ensure documentation accurately reflects the barter nature and fair market value for customs purposes. At DocShipper, we specialize in preparing compliant documentation for countertrade operations.

Yes. Hybrid arrangements where one party provides goods plus cash are common. These "partial barter" transactions require clear documentation separating the goods exchange value from the monetary component for accurate tax and customs reporting.

Direct barter eliminates exchange rate risk since no currency conversion occurs. However, if the contract references a currency for valuation purposes, fluctuations between agreement signing and delivery may require renegotiation unless the contract includes price adjustment clauses.

The WTO Customs Valuation Agreement provides guidelines for transaction value determination. Most countries follow these principles, requiring valuation based on comparable market transactions. Professional appraisal standards (USPAP, IVS) offer additional frameworks for complex goods.

Breach of contract remedies apply as with any commercial agreement. Well-drafted countertrade contracts specify liquidated damages, alternative performance options, or arbitration procedures. Escrow arrangements using third-party warehouses can secure performance for high-value exchanges.

Need Help with

Logistics or Sourcing ?

First, we secure the right products from the right suppliers at the right price by managing the sourcing process from start to finish. Then, we simplify your shipping experience - from pickup to final delivery - ensuring any product, anywhere, is delivered at highly competitive prices.

Fill the Form

Prefer email? Send us your inquiry, and we’ll get back to you as soon as possible.

Contact us

{kind=link}