In short ⚡

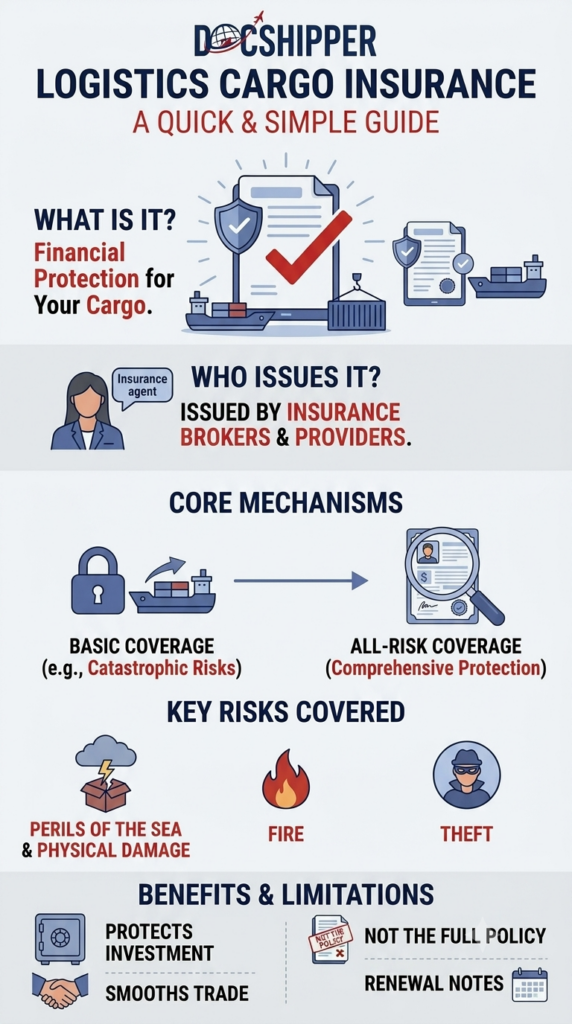

Insurance is a contractual mechanism that transfers financial risk from an individual or business to an insurance company in exchange for premium payments. In international logistics, cargo insurance protects against loss, damage, or theft during transportation, ensuring businesses recover financially from unforeseen events throughout the supply chain.

Introduction

Many businesses underestimate the financial exposure during international shipments. A single incident—container loss at sea, warehouse fire, or customs seizure—can wipe out profits or even threaten business continuity.

Insurance in logistics serves as the safety net that transforms unpredictable risks into manageable costs. Whether shipping electronics from China or machinery to Brazil, proper coverage ensures you’re protected against the countless variables in global trade.

Key characteristics of logistics insurance include:

- Risk transfer: Financial burden shifts from shipper to insurer

- Premium-based: Cost calculated on cargo value, route, and risk factors

- Contractual coverage: Specific terms define what’s protected and excluded

- Claims process: Documented procedure to recover losses

- International frameworks: Governed by conventions like the Institute Cargo Clauses

Insurance Mechanisms & Expertise in Freight

Understanding cargo insurance structures is essential for import-export operations. The insurance landscape divides into distinct coverage levels, each addressing different risk appetites and shipment characteristics.

Institute Cargo Clauses (ICC) form the international standard. ICC “A” provides all-risk coverage, protecting against virtually any loss except willful misconduct. ICC “B” covers specific named perils like fire, explosion, and vessel collision. ICC “C” offers the most restrictive coverage, limited to major casualties only.

The insurable interest principle requires the policyholder to have legitimate financial stake in the cargo. You cannot insure goods you don’t own or have no monetary interest in. This prevents speculative insurance fraud.

Valuation methods determine claim payouts. CIF (Cost, Insurance, Freight) value typically adds 10% to invoice value, covering profit margin and additional costs. Open declarations allow regular shippers to report shipments under master policies, streamlining administration.

Exclusions and limitations define boundaries. Standard policies exclude inherent vice (natural deterioration), improper packing, delay, and war risks unless specifically added. Understanding these gaps prevents nasty surprises during claims.

At DocShipper, we systematically review insurance certificates against shipment details, ensuring coverage matches cargo value and route risks before departure. According to International Trade Administration, proper insurance documentation expedites customs clearance and demonstrates due diligence in case of disputes.

Concrete Examples & Data

Real-world scenarios illustrate how insurance choices impact bottom lines. Consider these comparative cases that demonstrate the financial stakes:

| Scenario | Coverage Type | Loss Event | Claim Result |

|---|---|---|---|

| Electronics shipment ($150,000) | ICC “A” All-Risk | Container water damage during storm | $147,500 recovered (98% claim) |

| Same electronics shipment | ICC “C” Basic | Same water damage event | $0 recovered (storm not named peril) |

| Textile shipment ($80,000) | No insurance | Warehouse fire at destination | Total loss + business disruption |

| Machinery ($250,000) | ICC “A” + War Risk | Vessel seizure in conflict zone | $245,000 recovered (2% deductible) |

Cost-benefit analysis: Premium rates typically range from 0.2% to 2% of cargo value depending on commodity, route, and coverage level. For a $100,000 shipment, comprehensive ICC “A” coverage might cost $500-$1,000, while basic ICC “C” could be $200-$400.

Claims statistics reveal patterns. Industry data shows 15-20% of ocean freight containers experience some form of damage during transit, though most incidents are minor. However, total losses—though rare at 0.1% of shipments—can be catastrophic without insurance.

Use case: A European importer orders $200,000 worth of consumer electronics from Vietnam. They opt for ICC “A” coverage at 0.8% premium ($1,600). During transshipment in Singapore, forklift operators drop a pallet, damaging $35,000 worth of goods. The insurance claim recovers $34,300 after a $700 deductible—protecting the importer’s profit margin and customer commitments.

DocShipper clients who utilize our insurance coordination services experience 40% faster claims processing due to pre-verified documentation and direct insurer relationships. We match coverage to specific cargo risks, eliminating over-insurance costs while ensuring adequate protection.

Conclusion

Insurance transforms international shipping from a gamble into a calculated business process. The right coverage protects your investment, maintains cash flow, and ensures supply chain resilience against inevitable disruptions.

Need expert guidance on cargo insurance for your shipments? Contact DocShipper for personalized coverage recommendations and seamless insurance coordination.

📚 Quiz

Test Your Knowledge: Insurance in International Trade

What is the primary function of cargo insurance in international logistics?

A shipper transports electronics under CIF terms with the seller's insurance. Which statement is correct?

A container suffers water damage during a storm. The cargo was insured under ICC "C" basic coverage. What is the likely outcome?

🎯 Your Result

📞 Free Quote in 24hFAQ | Insurance: Definition, Types & Concrete Examples in International Trade

Carrier liability is the legal responsibility of the shipping company, typically limited to minimal amounts (e.g., $2 per kilogram under Montreal Convention for air freight). Cargo insurance is separate commercial coverage you purchase for full cargo value protection. Carrier liability rarely covers actual loss amounts—dedicated insurance fills this gap.

CIF (Cost, Insurance, Freight) means the seller arranges insurance, but only minimum coverage (typically ICC "C"). As the buyer, you should verify coverage adequacy and consider supplemental insurance if the cargo value is high or risks substantial. The seller's policy may not protect your full interests.

Most policies require notification within 48-72 hours of discovering damage and formal claims within 30-90 days. Document everything immediately: photographs, packing lists, carrier damage reports, and independent surveys. Delayed claims face rejection or reduced settlements.

ICC "A" all-risk policies cover natural disasters like earthquakes, floods, and hurricanes unless specifically excluded. ICC "B" and "C" have more restrictions—always read policy schedules. War risks, strikes, and terrorism typically require separate endorsements regardless of base coverage.

Sue and labor clauses require you to take reasonable steps to minimize loss after an incident occurs. If your container is damaged but goods are salvageable, you must arrange recovery. Insurers reimburse these mitigation costs separately from the claim itself—proactive action protects your full recovery rights.

No. Insurance requires goods to be in sound condition at policy inception. Pre-existing damage must be disclosed and will be excluded from coverage. Insurers may inspect high-value shipments before binding coverage to verify condition and proper packing.

Premiums depend on cargo value, commodity type (electronics cost more than textiles), route risk (piracy zones increase rates), packing quality, shipping mode, and claims history. High-value or fragile goods in high-risk regions command premium rates of 1-3%, while low-risk bulk commodities might be 0.1-0.3%.

Essential documents include the original insurance certificate, commercial invoice, packing list, bill of lading or air waybill, damage survey report, photographs, carrier's damage acknowledgment, and correspondence proving claim notification timeline. Missing documentation causes claim delays or denials.

Yes. Port-to-port (CIF/CIP) covers only the main carriage. Door-to-door (warehouse-to-warehouse) extends coverage through inland transport, storage, and handling before vessel loading and after discharge. For complete protection through the entire logistics chain, specify warehouse-to-warehouse coverage in your policy.

Standard cargo insurance excludes losses from customs violations, regulatory non-compliance, or government seizures. If goods are confiscated due to incorrect documentation, prohibited items, or sanctions violations, insurers won't pay. Specialized trade disruption insurance exists but requires separate underwriting.

Frequent shippers benefit from annual open policies—you declare shipments as they occur under pre-negotiated terms and rates. Occasional importers find per-shipment policies more economical. Annual policies typically offer 15-25% cost savings for businesses with consistent shipping volumes and streamline administration significantly.

Deductibles range from $500 to $5,000 per claim or 1-5% of claim value, whichever is greater. Higher deductibles reduce premium costs but increase out-of-pocket exposure for minor incidents. Businesses must balance premium savings against risk tolerance—frequent small claims favor low deductibles despite higher premiums.

Need Help with

Logistics or Sourcing ?

First, we secure the right products from the right suppliers at the right price by managing the sourcing process from start to finish. Then, we simplify your shipping experience - from pickup to final delivery - ensuring any product, anywhere, is delivered at highly competitive prices.

Fill the Form

Prefer email? Send us your inquiry, and we’ll get back to you as soon as possible.

Contact us

{kind=link}