In short ⚡

Marine Cargo Insurance – Average refers to the principle of loss apportionment in maritime transport. It encompasses two types: General Average, where all cargo interests proportionally share costs from voluntary sacrifices made for common safety, and Particular Average, covering partial losses to specific cargo. This fundamental maritime law concept determines financial responsibility when goods are damaged or sacrificed during sea transit.

Introduction

Confusion surrounding “average” in marine insurance costs importers thousands annually in unexpected claims. Unlike standard insurance terminology, “average” doesn’t mean typical or ordinary – it describes a complex system of loss distribution dating back centuries of maritime law.

In international trade, understanding average clauses determines whether you’ll face surprise invoices after shipment incidents. The distinction between General Average and Particular Average fundamentally affects your financial exposure and insurance requirements.

Key characteristics of marine cargo average include:

- Historical Origin: Rooted in ancient maritime codes like the Rhodian Sea Law (800 BC)

- Dual Classification: General Average (shared sacrifice) vs. Particular Average (individual loss)

- Proportional Liability: Calculated based on cargo value ratios

- Declaration Requirements: Vessel masters must formally declare General Average events

- Insurance Coverage: Policies vary significantly in average protection levels

Understanding Average Principles & Legal Framework

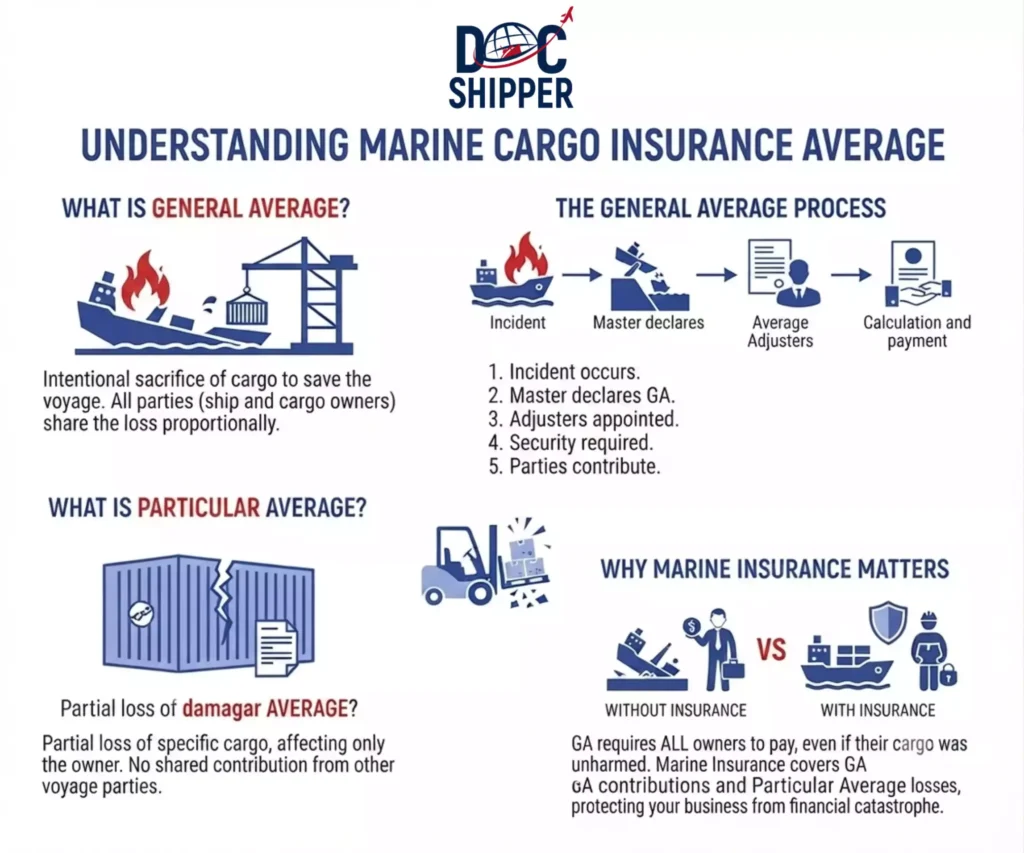

General Average represents one of maritime law’s oldest principles. When a vessel faces imminent peril, the captain may deliberately sacrifice cargo or incur expenses to save the voyage. All parties with interests in the voyage – shipowner, various cargo owners – proportionally share these costs.

For General Average to apply, four conditions must exist: common maritime adventure (shared journey), real and imminent danger, voluntary sacrifice (deliberate decision), and successful preservation (some property saved). Classic examples include jettisoning containers during storms or emergency port diversions.

Particular Average covers partial losses affecting specific cargo without benefiting other interests. Sea water damage to one container represents Particular Average – only that cargo owner bears the loss. This contrasts sharply with General Average’s shared responsibility model.

The York-Antwerp Rules, established in 1890 and regularly updated (latest 2016), standardize General Average calculations internationally. Most bills of lading reference these rules, creating uniform interpretation across jurisdictions. At DocShipper, we systematically review insurance certificates to verify adequate average coverage before shipments depart.

Average adjusters – specialized professionals – calculate contribution percentages when General Average is declared. This process typically takes 12-24 months, during which cargo may be held as security. The official York-Antwerp Rules framework governs these complex calculations globally.

Insurance policies offer three main coverage levels: Free of Particular Average (FPA) covers only total losses and General Average, With Average (WA) includes Particular Average above certain percentages, and All Risks provides broadest protection. Understanding these distinctions prevents costly coverage gaps.

Practical Scenarios & Financial Calculations

Consider a container vessel carrying mixed cargo worth $10 million facing engine fire mid-ocean. The captain jettisons $500,000 worth of containers to stabilize the ship and incurs $300,000 in emergency port expenses. Total General Average sacrifice: $800,000.

| Party | Cargo Value | Percentage | Contribution Due |

|---|---|---|---|

| Importer A (Electronics) | $2,000,000 | 20% | $160,000 |

| Importer B (Textiles) | $3,000,000 | 30% | $240,000 |

| Importer C (Machinery) | $5,000,000 | 50% | $400,000 |

| TOTAL | $10,000,000 | 100% | $800,000 |

Even if Importer C’s machinery remained untouched, they contribute $400,000 because the sacrifice benefited all cargo. Without adequate insurance, this becomes an out-of-pocket expense.

Particular Average scenario: A refrigerated container suffers mechanical failure, spoiling $80,000 worth of pharmaceuticals. No other cargo is affected. Under FPA coverage, the importer receives nothing. With WA coverage (typically 3% franchise), if the loss exceeds 3% of insured value ($2,400), the full $80,000 is recoverable.

Statistical data reveals General Average declarations occur in approximately 1 in 200 ocean voyages, with average settlement values ranging from $50,000 to $5 million. Container jettisoning represents 35% of cases, fire/explosion 28%, and groundings 22%.

DocShipper encountered a case where a client shipping automotive parts faced unexpected $127,000 General Average contribution after a vessel grounding near Suez Canal. Their inadequate insurance (FPA only) left them personally liable, delaying delivery by 18 months during adjuster negotiations.

Coverage comparison reveals: FPA policies cost 30-40% less than All Risks but exclude 70% of common marine losses. For high-value or time-sensitive cargo, the premium difference becomes negligible compared to potential exposure.

Conclusion

Marine Cargo Insurance Average principles – whether General or Particular – fundamentally determine financial responsibility when maritime incidents occur. Understanding coverage distinctions prevents unexpected liabilities that can devastate profit margins or strand cargo indefinitely.

Need guidance navigating marine insurance complexities for your shipments? Contact DocShipper’s insurance specialists for comprehensive coverage analysis tailored to your cargo profile.

📚 Quiz

Test Your Knowledge: Marine Cargo Insurance – Average

What does "average" mean in marine cargo insurance terminology?

Your $2M cargo arrives undamaged, but the vessel jettisoned other containers during a storm to save the ship. Are you liable for General Average contributions?

An importer with FPA (Free of Particular Average) coverage experiences seawater damage worth $60,000 to their container. What happens?

🎯 Your Result

📞 Free Quote in 24hFAQ | Marine Cargo Insurance – Average: Definition, Calculation & Concrete Examples

A vessel master declares General Average when deliberate sacrifice or extraordinary expenses are incurred to save the ship and cargo from imminent peril. This requires real danger (not theoretical risk), voluntary action (intentional decision), and successful outcome (some property preserved). Common triggers include jettisoning cargo during storms, emergency towing, fire suppression costs, or refuge port expenses after machinery failure.

Yes, absolutely. General Average contributions are based on your cargo's proportional value to the total adventure, regardless of whether your specific goods were sacrificed or damaged. If your $500,000 shipment represents 10% of total cargo value, you contribute 10% of all General Average expenses. This centuries-old principle ensures fair distribution of costs for actions benefiting all parties.

Average adjusters typically require 12-24 months to complete calculations, though complex cases extend to 36 months. During this period, cargo may be held as security until you provide a General Average bond or guarantee. This delay significantly impacts cash flow and inventory planning. Adequate insurance with automatic General Average coverage eliminates these complications entirely.

Free of Particular Average (FPA) covers only total losses and General Average contributions – not partial damage to your specific cargo. "All Risks" provides comprehensive protection including Particular Average (partial losses), theft, contamination, and most accidental damages. For high-value shipments, All Risks costs only 15-25% more than FPA but covers scenarios representing 70% of actual marine claims.

Legally, no. Bills of lading incorporate General Average clauses making contributions contractually obligatory. Refusal results in cargo detention at destination until payment or security is provided. Carriers possess maritime liens on cargo for General Average debt. Litigation costs typically exceed the contribution itself, making insurance the only practical solution.

Only if referenced in your transport contract, which most standard bills of lading include. The 2016 York-Antwerp Rules provide standardized calculation methods, but older versions (1994, 2004) may apply depending on contract terms. Always verify which rule version governs your shipment, as calculation methodologies differ. Containers shipped under charter parties may operate under different frameworks entirely.

With Average policies typically include a franchise clause – commonly 3% of insured value. If damage exceeds this threshold, the entire loss is recoverable; below it, nothing is paid. Some policies use "deductible" structures where the percentage is subtracted from all claims. Always clarify whether your policy operates on franchise (threshold) or deductible (reduction) basis.

Generally no. Marine insurance average principles apply specifically to ocean and coastal voyages under maritime law. Inland waterway transport (rivers, canals) operates under different legal frameworks with separate insurance structures. However, combined transport policies covering sea-to-inland legs may incorporate average clauses for the maritime portion. Always verify coverage scope with your insurer.

Average adjusters determine each party's "contributory value" – the cargo's sound arrival value minus any Particular Average losses. They sum all contributory values (including vessel value) to establish the total. Your contribution percentage equals your contributory value divided by this total, multiplied by total allowable General Average expenses. Professional adjusters follow York-Antwerp Rules methodologies ensuring consistent international treatment.

Modern shipping sees approximately 1,500 containers lost overboard annually worldwide, with deliberate jettisoning representing 30-40% of cases. While individual voyage probability remains low, high-volume shippers face mathematical certainty of eventual exposure. The 2021 Ever Given Suez blockage generated estimated $600 million in General Average claims, demonstrating the scale of potential liability even without cargo loss.

Theoretically possible but practically impossible with common carriers using standard bills of lading. General Average clauses are fundamental to maritime law and carrier liability limitations. Charter party arrangements may offer negotiation flexibility, but carriers typically refuse to assume disproportionate risk. Comprehensive insurance represents the only reliable protection method accepted across the industry.

You remain liable only for your proportional contribution regardless of others' payment capacity. If parties default, the shortfall is absorbed by those who suffered the sacrifice (whose cargo was jettisoned or damaged). This doesn't increase your contribution percentage. However, settlement delays may extend while adjusters pursue non-paying parties through legal channels.

Need Help with

Logistics or Sourcing ?

First, we secure the right products from the right suppliers at the right price by managing the sourcing process from start to finish. Then, we simplify your shipping experience - from pickup to final delivery - ensuring any product, anywhere, is delivered at highly competitive prices.

Fill the Form

Prefer email? Send us your inquiry, and we’ll get back to you as soon as possible.

Contact us

{kind=link}