In short ⚡

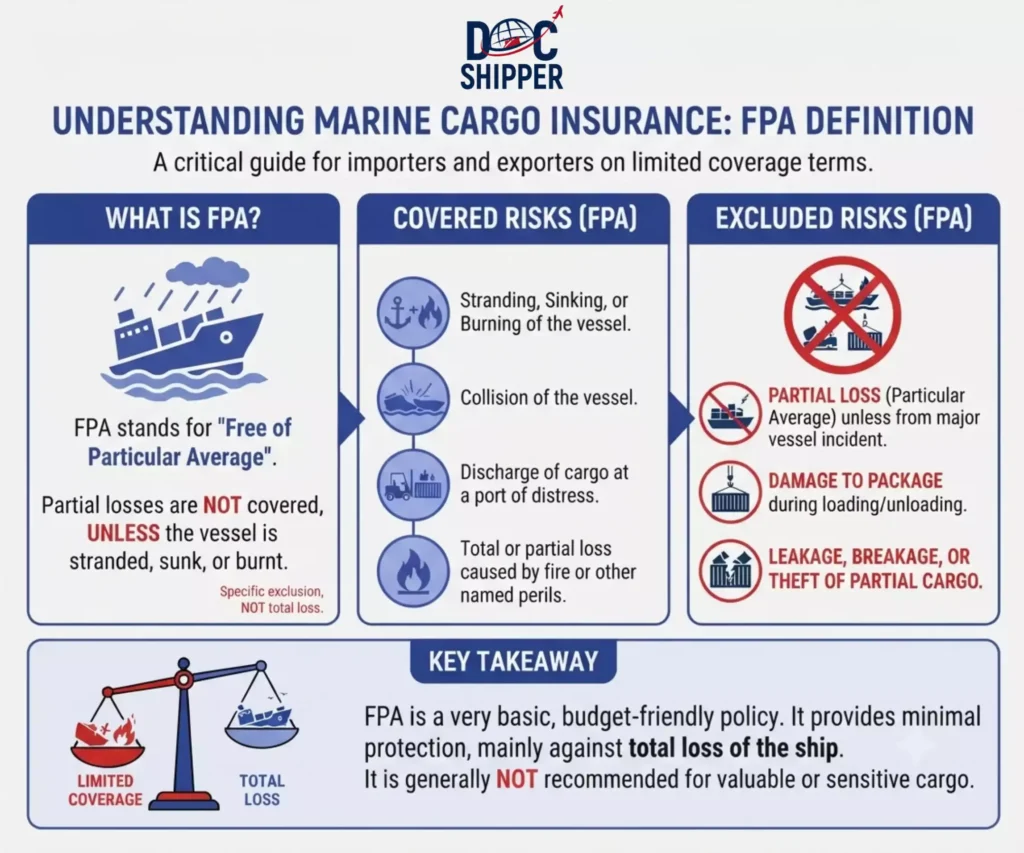

Marine Cargo Insurance – FPA (Free of Particular Average) is a restrictive marine insurance clause providing coverage only for total losses and specified major perils, excluding partial damage claims. This coverage protects shipments against catastrophic events like vessel sinking or fire, but not minor incidents during transit.

Introduction

Many importers assume all marine insurance policies cover any damage occurring during sea transport. This misconception leads to unpleasant surprises when partial loss claims are denied under FPA coverage. Understanding the limitations of Free of Particular Average insurance is critical for international trade risk management.

In global logistics, the choice between FPA and broader coverage determines your financial exposure. FPA represents the most basic level of marine cargo protection, designed for low-risk commodities or budget-conscious shippers willing to self-insure partial losses.

Key characteristics of FPA coverage include:

- Total loss protection when the entire shipment is destroyed or becomes a constructive total loss

- Major peril coverage including fire, explosion, vessel collision, and stranding

- General average contributions are covered when declared during a maritime emergency

- Exclusion of partial damage from water, contamination, or minor handling incidents

- Lower premium rates compared to All Risks or WPA (With Particular Average) policies

Understanding FPA Coverage & Legal Framework

The FPA clause originated in 18th-century Lloyd’s of London practices when maritime risks were poorly understood. The term “particular average” refers to partial losses borne by individual cargo owners, as opposed to “general average” where all parties share salvage costs proportionally.

Under FPA terms, insurers only compensate for actual total loss (complete destruction or disappearance of goods) and constructive total loss (when recovery costs exceed cargo value). The policy explicitly covers five major named perils: vessel sinking, capsizing, fire/explosion, collision with external objects, and discharge at a distress port following these events.

The legal foundation for FPA coverage comes from the UK Marine Insurance Act 1906, which remains the benchmark for international marine insurance contracts. Section 56 specifically addresses particular average losses and their exclusions under FPA terms.

General average contributions represent a unique exception to FPA limitations. When a ship’s captain makes voluntary sacrifices to save the voyage (jettisoning cargo, seeking refuge port), all stakeholders contribute proportionally. FPA policies cover your share of these declared general average expenses, even though they constitute partial losses.

Important exclusions under FPA include water damage from leakage, contamination, theft, breakage during handling, and losses from inherent vice (natural deterioration). These exclusions make FPA unsuitable for fragile, high-value, or perishable commodities requiring comprehensive protection.

At DocShipper, we systematically review clients’ cargo profiles before recommending FPA coverage. For bulk commodities like coal, ore, or grain with low damage susceptibility, FPA offers cost-effective basic protection. However, we advise upgrading to WPA or All Risks for manufactured goods, electronics, and temperature-sensitive products.

Practical Scenarios & Cost Comparison

Consider a container shipment of ceramic tiles valued at $50,000 traveling from Shanghai to Rotterdam. Under different insurance scenarios, the coverage outcomes vary dramatically:

| Incident Type | FPA Coverage | WPA Coverage | All Risks |

|---|---|---|---|

| Vessel sinks (total loss) | $50,000 paid | $50,000 paid | $50,000 paid |

| Container water ingress ($8,000 damage) | $0 (excluded) | $8,000 paid | $8,000 paid |

| Crane drop during loading ($12,000 damage) | $0 (excluded) | $0 (excluded) | $12,000 paid |

| Container fire on deck ($50,000 loss) | $50,000 paid | $50,000 paid | $50,000 paid |

| Theft of 3 pallets ($4,500 loss) | $0 (excluded) | $0 (excluded) | $4,500 paid |

| Premium cost estimate | $125 (0.25%) | $200 (0.40%) | $350 (0.70%) |

This comparison illustrates why FPA suits only 15-20% of containerized cargo in international trade. The premium savings appear attractive, but one partial loss incident negates years of accumulated savings.

Real-world case study: A mining company shipping iron ore from Brazil to China opted for FPA coverage on 200,000 metric tons across 15 voyages annually. Their commodity’s characteristics (non-perishable, bulk handling, low theft risk) aligned perfectly with FPA limitations. Over five years, they saved approximately $180,000 in premium costs without filing a single partial loss claim.

Conversely, an electronics manufacturer shipping laptop components suffered a $45,000 partial loss when seawater entered their container during rough weather. Their FPA policy denied the claim because the vessel itself remained seaworthy, categorizing it as particular average damage rather than a total loss scenario.

When evaluating FPA appropriateness for your shipments, consider these five critical factors:

- Cargo resilience: Non-fragile commodities withstand transport stress better

- Value concentration: Low-value bulk goods justify minimal insurance investment

- Historical loss patterns: Review past claims to identify vulnerability patterns

- Trade route stability: Established lanes with modern vessels reduce catastrophic risk

- Financial capacity: Your ability to absorb partial losses without operational disruption

At DocShipper, we analyze these variables during our freight forwarding consultations to recommend coverage matching your risk profile and budget constraints.

Conclusion

Marine Cargo Insurance – FPA provides essential catastrophic loss protection while excluding routine partial damage claims. This coverage suits resilient commodities where premium savings outweigh self-insurance risks for minor incidents.

Need expert guidance on marine insurance selection for your international shipments? Contact DocShipper’s insurance specialists for a customized risk assessment and coverage recommendation.

📚 Quiz

Test Your Knowledge: FPA Marine Cargo Insurance

What does "Free of Particular Average" coverage primarily protect against?

A container suffers $10,000 water damage when seawater enters through a seal breach during rough weather, but the vessel remains seaworthy. Under FPA coverage, what happens?

Which commodity type is MOST suitable for FPA insurance coverage?

🎯 Your Result

📞 Free Personalized QuoteFAQ | Marine Cargo Insurance – FPA (Free of Particular Average): Definition, Coverage & Practical Examples

The term indicates the insurer is "free" (exempt) from paying "particular average" (partial loss claims affecting individual cargo owners). Only total losses and specified major perils trigger compensation under FPA terms, making it the most restrictive standard marine coverage option available.

Yes, FPA premiums typically cost 40-60% less than All Risks policies. For a $100,000 shipment, FPA might cost $250 (0.25%) while All Risks reaches $700 (0.70%). However, this economy comes with significant coverage limitations that may prove costly if partial damage occurs during transit.

Generally no. FPA excludes water damage from leakage, rain, or seawater ingress unless the vessel itself is lost, stranded, sunk, or destroyed by fire. Minor water intrusion affecting only your cargo without threatening the vessel falls outside FPA coverage parameters.

Bulk raw materials like coal, iron ore, grains, crude oil, and minerals work well with FPA coverage. These commodities resist minor handling damage, have relatively low per-unit values, and primarily face catastrophic loss risks rather than partial damage scenarios during ocean transport.

Yes, FPA policies explicitly cover your proportionate share of declared general average expenses. When a ship's captain makes extraordinary sacrifices to save the voyage (jettisoning cargo, emergency port costs), all parties contribute based on saved value, and FPA insurers honor these obligations despite excluding other partial losses.

Yes, if your container is lost overboard during the voyage, this constitutes an actual total loss covered by FPA terms. However, if the container is recovered with damaged contents, you cannot claim for that internal damage as it represents particular average rather than total loss.

WPA (With Particular Average) covers partial losses exceeding a specified percentage (typically 3-5% of insured value), plus all FPA-covered perils. FPA only covers total losses and major named perils, excluding routine partial damage claims regardless of percentage. WPA premiums run approximately 50-80% higher than FPA rates.

No, FPA excludes theft, pilferage, and non-delivery unless they occur as direct consequences of a covered major peril like vessel sinking or fire. If cargo disappears during normal port handling or container stuffing, FPA policies deny these claims as particular average losses outside coverage scope.

Constructive total loss occurs when salvage, repair, and forwarding costs would exceed the cargo's delivered value. Professional surveyors assess damage after incidents to determine whether repair is economically viable. If costs exceed insured value, insurers treat it as total loss and settle accordingly under FPA terms.

No, marine insurance policies attach at cargo movement commencement and cannot be upgraded retroactively. You must arrange appropriate coverage before the voyage begins. If your shipment departs with FPA coverage, that remains the applicable policy until destination arrival, regardless of changed risk perceptions during transit.

FPA covers natural disasters (storms, lightning strikes) only if they result in total loss or trigger covered major perils like vessel sinking or stranding. Minor damage from rough seas, humidity, or temperature fluctuations causing partial cargo deterioration falls outside FPA coverage as particular average losses.

Absolutely not. Electronics face substantial partial damage risks from moisture, handling impacts, and vibration during transit. FPA's exclusion of these common risks makes it inappropriate for fragile, high-value goods. All Risks or WPA coverage provides necessary protection for electronics, pharmaceutical products, and precision machinery shipments.

Need Help with

Logistics or Sourcing ?

First, we secure the right products from the right suppliers at the right price by managing the sourcing process from start to finish. Then, we simplify your shipping experience - from pickup to final delivery - ensuring any product, anywhere, is delivered at highly competitive prices.

Fill the Form

Prefer email? Send us your inquiry, and we’ll get back to you as soon as possible.

Contact us

:%20Definition,%20Coverage%20&%20Practical%20Examples){kind=link}